In an effort to stabilize the financial system, the Monetary Authority of Singapore (MAS) has introduced a series of lending rules, which, for shorthand purposes, are collectively referred to as Cooling Measures or just TDSR by the general public.

TDSR stands for Total Debt Servicing Ratio and is part of an effort by MAS to standardize the mortgage underwriting process.

Underwriting is a fancy way of saying that the banks are trying to figure out whether or not you will repay the loan.

When you apply for a mortgage, the bank will typically consider your credit score, capacity to pay, and the value of the home. These are known as the three “C’s” of mortgage underwriting.

Your credit score accounts for your ability to pay back loans, including credit card debt, car loans, other home mortgages, and personal loans.

Bank underwriters look at your income, existing debt, and your employment history to evaluate your capacity to pay back the loan according to its terms and conditions.

Finally, banks examine the collateral behind the loan, which in the case of a mortgage is the home itself. In event of default, bankers want to know at what price they can resell the property.

By standardizing underwriting, MAS is making it easier for banks to regulate and measure risk in their mortgage portfolios. This, in turns, helps to strengthen the overall financial stability of the nation.

At the same time, though, MAS lending rules cap how much households can borrow. Standardizing underwriting has a knock-on effect in that it dictates what type of properties families can finance.

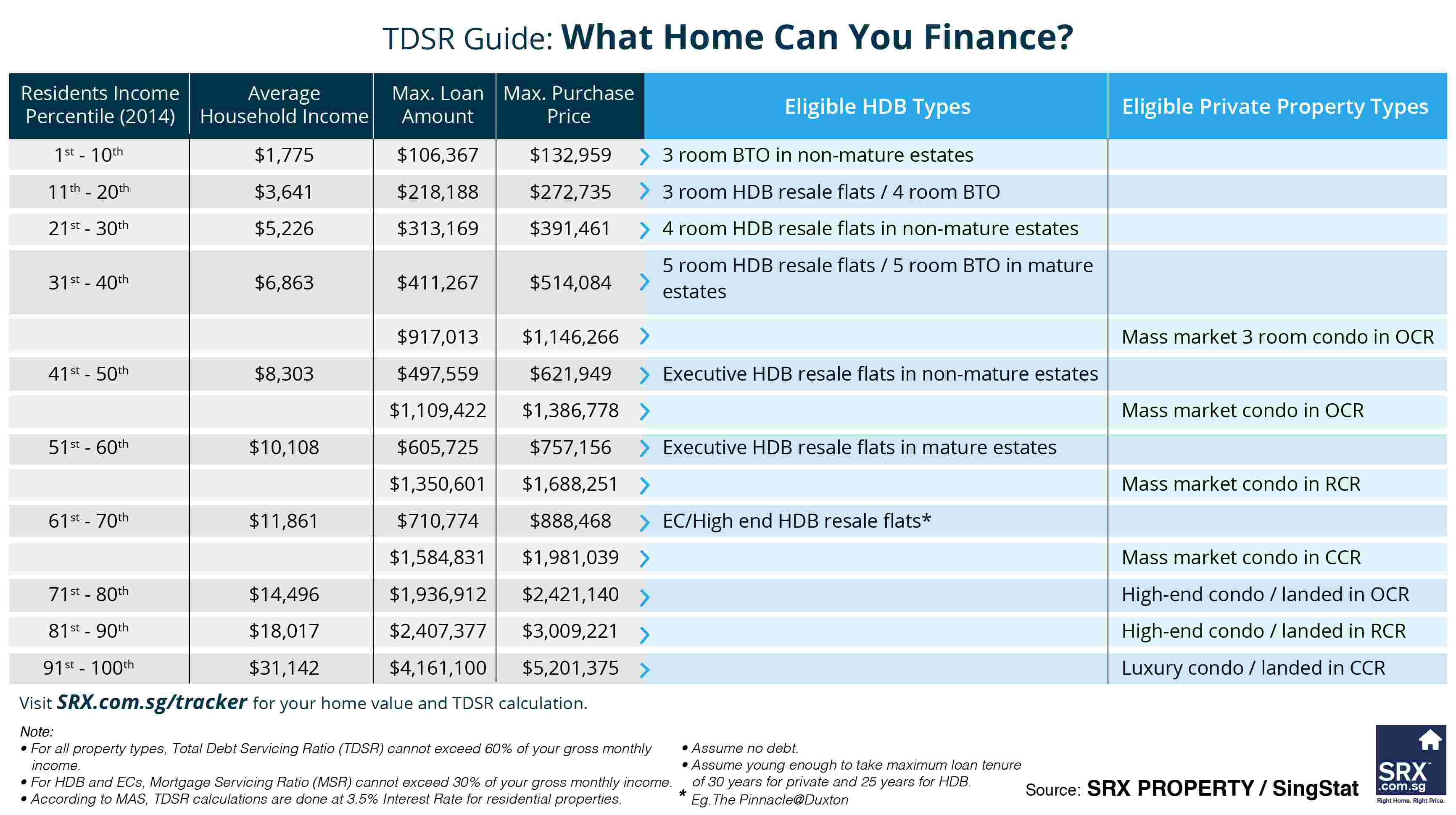

In an effort to help people understand what type of property one can finance for each income percentile, SRX Property has put together a TDSR Guide.

The table shows the maximum loan, purchase price, and eligible property types for each income percentile, as defined by Singapore Statistics.

In calculating the different loan amounts for each income percentile, we assume no debt. TDSR limits the amount of allowable consumer debt to 60% of household income.

In the case of HDB loans, mortgage debt cannot exceed 30%. (This is known as MSR - the Mortgage Servicing Ratio.)

Also, MAS rules regulate the loan-to-value ratio (LTV). For example, the LTV ratio for primary home loans is 80%. This means that for a $1 million purchase price, the borrower must put down $200,000 (or 20%) to borrow $ 800,000 (or 80%).

In the case of a second home the LTV can become 50%, which means $500,000 cash outlay.

For calculation purposes, we assume an LTV of 80%. Also, we assume maximum loan tenure of 25 years for HDB and 30 years for private homes.

The table is interesting in that it reveals about 60% of Singaporeans qualify for financing private homes under MAS rules.

Also, it shows that the same income qualifies you for a higher loan if you are buying a private home as opposed to an HDB.

For example, if your household earns $8,303 per month, you can qualify for a maximum HDB loan amount of $ 497,559. This translates to a maximum purchase price of $621,949, which makes you eligible for Executive HDB flats.

At the same time, you are can qualify for a loan for a private home up to $1,109,422. This translates to a maximum purchase price of $1,386,778 and makes you eligible for a mass market condo in OCR.

The reason for this anomaly is that HDB has stricter lending requirements. Specifically, the loan tenure of 25 years for HDB means a higher monthly loan repayment, which, in turn, requires higher household income.

Also, MSR, which applies only to HDB financing, means you cannot borrow as great a percentage of your income as would be the case if you were purchasing a private home..

While MAS rules do place limits on bank lending, it is very clear what types of properties you can finance. Each listing page on SRX.com.sg and my Property Tracker contain the TDSR Guide and a calculator for you to compute what you can borrow given your financial circumstances.

Now, all that is left to do is to find the right home at the right price within your specific income segment.