Singapore's New Property Market Cooling Measures, Latest Updates 2023

The ABSD rate will depend on the buyer profile as at the date of purchase or acquisition of the residential unit. Hide

| Citizenship | ABSD Rate on Primary Home Purchase |

ABSD Rate on Secondary Home Purchase |

ABSD Rate on Tertiary & Subsequent Purchase |

|---|---|---|---|

| Singapore Citizens | N/A | 17% revised to 20% | 25% revised to 30% |

| Permanent Residents | remains unchanged at 5% | 25% revised to 30% | 30% revised to 35% |

| Foreigners1 | 30% revised to 60% | 30% revised to 60% | 30% revised to 60% |

| Corporate Entities | 35% revised to 65% | 35% revised to 65% | 35% revised to 65% |

| Date of Purchase | Year 1 | Year 2 | Year 3 | Year 4 |

|---|---|---|---|---|

| Between 20 Feb 2010 and 29 Aug 2010 | Same as basic Buyer Stamp Duty |

N/A | N/A | N/A |

| Between 30 Aug 2010 and 13 Jan 2011 | Same as basic Buyer Stamp Duty |

2/3 of basic Buyer Stamp Duty |

1/3 of basic Buyer Stamp Duty |

N/A |

| Between 14 Jan 2011 and 10 Mar 2017 | 16% | 12% | 8% | 4% |

| On and after 11 Mar 2017 | 12% | 8% | 4% | N/A |

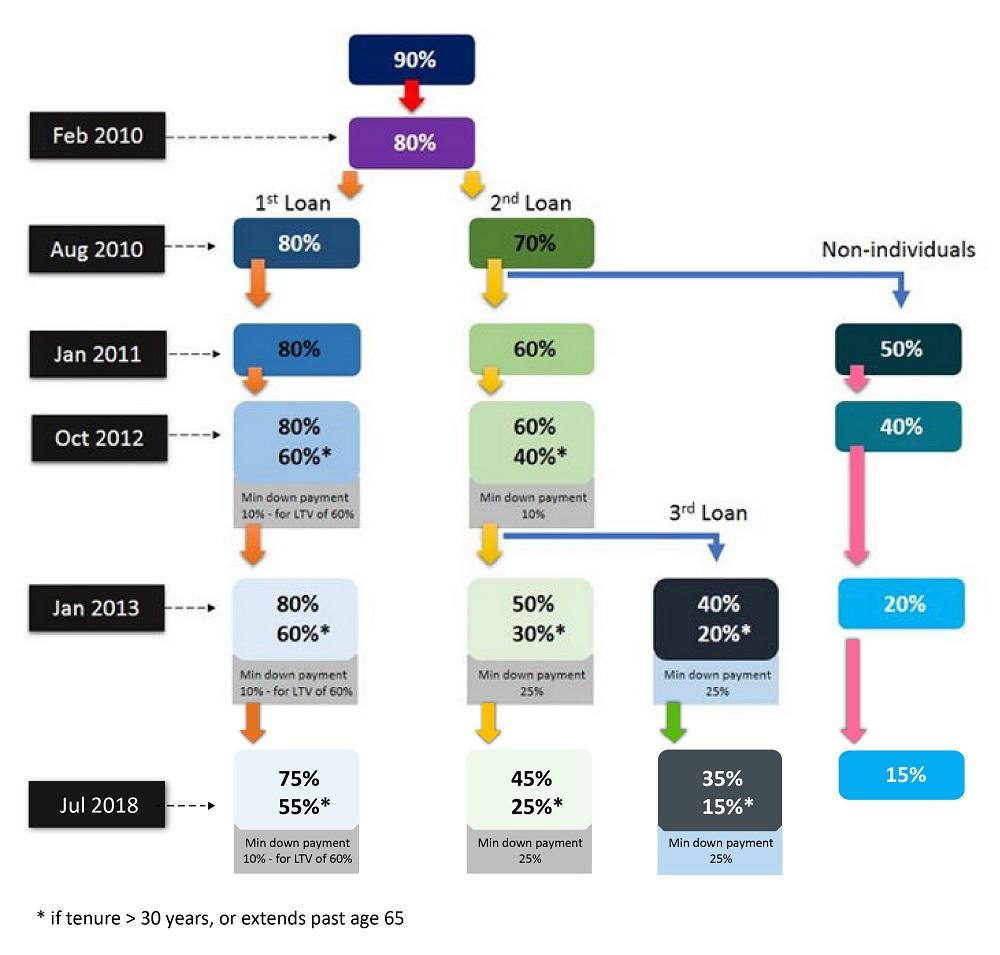

With effect from 30 September 2022, the LTV limit for HDB housing loans was lowered by 5% from 85% to 80%. The revised LTV limit does not apply to loans granted by financial institutions, for which the LTV limit remains at 75%.

| Effective Date | Major Cooling Measures that Affect Residential Property Market |

|---|---|

| 27 April 2023 | 1. ABSD rates for Singaporeans increased from 17% to 20% for purchasing their second residential property and from 25% to 30% for third and subsequent properties; ABSD rates for SPRs increased from 25% to 30% for purchasing their second residential property and from 30% to 35% for third and subsequent properties; ABSD rates for Singaporeans and SPRs purchasing their first residential property will remain unchanged at 0% and 5% respectively; ABSD rates for foreigners increased from 30% to 60% for the purchase of any residential property. |

| 15 February 2023 | 1. BSD rates increased for higher-value properties; the portion of a property's value in excess of S$1.5 million and up to S$3 million will be taxed at 5%, while those in excess of S$3 million will be taxed at 6%. |

| 30 September 2022 | 1. Higher medium-term interest rate floor for bank and HDB housing loan eligibility. From 30 September 2022, banks will calculate applicants' TDSR and MSR from a new medium-term interest rate - such as the higher 4% per annum floor or thereafter interest rate (for residential property purchase loans and mortgage equity withdrawal). For housing loans granted by HDB, HDB will introduce an interest rate floor of 3% for computing eligible loan amounts. |

| 2. Lowered LTV limit for HDB-granted loans from 85% to 80%. | |

| 3. 15-month wait for Private Property Owners (below 55 years old) buying non-subsidised HDB resale flat. | |

| 16 December 2021 | 1. ABSD rates for Singaporeans and SPRs purchasing their first residential property will remain unchanged at 0% and 5% respectively; For foreigners, their ABSD will be 30% for the purchase of any residential property; The rates for Singaporeans and SPRs buying their second and subsequent properties will be raised by 5% and 10% respectively while that for corporate entities will be increased by 10%. |

| 2. Tightened Total Debt Servicing Ratio (TDSR) threshold from 60% to 55%. | |

| 3. Reduced LTV limit for HDB-granted loans from 90% to 85%. | |

| 06 July 2018 | 1. ABSD rates for Singaporeans and SPRs purchasing their first residential property will remain unchanged but their second and subsequent properties will be raised by 5%. Foreigners have to pay 5% more now which makes it 20% for any property purchase. For corporate entities, the rates increased by 10% and there's a new, non-remittable 5% ABSD for developers. |

| 2. LTV limits tightened by 5% for all housing loans granted by financial institutions. | |

| 11 March 2017 | 1. Seller Stamp Duty (SSD) reduced by 4% for each tier. With this change, SSD will only apply to properties sold within 3 years of purchase, down from 4 years previously. |

| 2. TDSR will not apply to mortgage equity withdrawal loans with Loan-to-Value (LTV) ratio equal or below 50%. | |

| 3. Introduced Additional Conveyance Duties (ACD) for Property Holding Equity (PHE). ACD plugs a loophole which exempted companies from paying ABSD and BSD in the past. A PHE is a company whose primary (i.e., > 50%) tangible assets are Singapore residential properties. | |

| 9 December, 2013 | 1. Reduction of Cancellation Fees From 20% to 5% for Executive Condominiums. |

| 2. Resale Levy for Second-Timer Applicants - Formerly second timers are not required to pay a levy. This is applicable to only new EC land sales which are launched on or after 9th December 2013. |

|

| 3. Revision of Mortgage Loan Terms - The MSR cap will apply to EC purchases from 10th December 2013 onwards. |

|

| 27 August, 2013 | 1. Singapore Permanent Resident Households need to wait three years from the date of obtaining SPR status, before they can buy a resale HDB flat. |

| 2. Maximum tenure for HDB housing loans is reduced from 30 years to 25 years. The Mortgage Servicing Ratio (MSR) limit is reduced from 35% to 30% of the borrower's gross monthly income. | |

| 3. Maximum tenure of new housing loans and re-financing facilities granted by financial institutions for the purchase of HDB flats (including DBSS flats) is reduced from 35 years to 30 years. News loans with tenure exceeding 25 years and up to 30 years will be subject to tighter LTV limits. | |

| 29 June, 2013 | 1. TDSR*: Financial institutions are required to consider borrowers' other outgoing debt obligations when granting property loans. His total monthly repayments of his debt obligations should not exceed 60 per cent of his gross monthly income. |

| 2. In particular, MAS requires: -borrowers named on a property loan to be the mortgagors of the residential property for which the loan is taken; -"guarantors" who are standing guarantee for borrowers otherwise assessed by the financial institutions at the point of application for the housing loan not to meet the TDSR threshold for a property loan to be brought in as co-borrowers; and -in the case of joint borrowers, that financial institutions use the income-weighted average age of borrowers when applying the rules on loan tenure. |

|

| 12 January, 2013 | 1. ABSD: Citizens pay 7/10% on second/third purchase (from 0/3%); Permanent Residents (PR) pay 5/10% for first/second purchase (from 0/3%); foreigners and non-individuals now pay 15%. |

| 2. LTV for second/third loan now 50/40% from 60%; non-individuals' LTV now 20% (from 40%). | |

| 3. Mortgage Servicing Ratio (MSR) for HDB loans now capped at 35% of gross monthly income (from 40%); MSR for loans from financial institutions capped at 30%. | |

| 4. PRs no longer allowed to rent out entire HDB flat. | |

| 6 October, 2012 | 1. Mortgage tenures capped at a maximum of 35 years. |

| 2. For loans longer than 30 years or for loans that extend beyond retirement age of 65 years: LTV lowered to 60% for first mortgage and to 40% for second and subsequent mortgages. | |

| 3. LTV for non-individuals lowered to 40%. | |

| 8 December, 2011 | 1. ABSD introduced for further cooling measures: -Foreigners and non-individuals pay 10%, PRs buying second and subsequent property pay 3%, Singaporeans buying third and subsequent property pay 3%. |

| 2. Developers purchasing more than four residential units and following through on intention to develop residential properties for sale would be waived ABSD -To qualify, developers have to produce proof of development and sale within five years. |

|

| 14 January, 2011 | 1. Holding period for imposition of SSD increased to four years from three. |

| 2. SSD rates raised to 16%, 12%, 8% and 4% of consideration. | |

| 3. LTV lowered to 60% from 70% for second property. | |

| 4. LTV for non-individual residential purchasers capped at 50%. | |

| 30 August, 2010 | 1. Holding period for imposition of SSD increased to three years from one. |

| 2. Minimum cash payments raised to 10% from 5% for buyers with one or more outstanding housing loans. | |

| 3. LTV lowered to 70% from 80% for second properties. | |

| 20 February, 2010 | 1. Introduction of SSD for residential property and land sold within one year of purchase. |

| 2. LTV lowered to 80% from 90% on all housing loans except HDB loans. | |

| 14 September, 2009 | 1. Interest absorption scheme (deferment of instalments until TOP) and interest-only housing loans (interest payment only until TOP) were scrapped for all private properties. |

The information contained in this document is the proprietary and exclusive property of StreeSine Singapore Pte. Ltd. (""SSPL"") except as otherwise indicated. The information contained herein is for informational purposes only and is not intended to replace any professional advice. The views expressed are entirely those of the authors.

Whilst the information is intended to be accurate and current, SSPL is not responsible for any errors or omissions in this document. SSPL may vary, withdraw or amend any information presented herein at any time without notice.

To the fullest extent permitted by law, in no event shall StreetSine, its officers and employees, affiliates, subsidiaries, successors and assigns be liable for any damages or costs, including without limitation any indirect, consequential, special, incidental, or punitive damages arising out of, based on, or resulting from your reliance on or use of the information herein.

No part of this document may be reproduced except as authorised by written permission. The copyright and the foregoing restriction extend to reproduction in all media.

©StreetSine Singapore Pte. Ltd. All rights reserved.

Singapore Real Estate Exchange Property Index, SPI, Singapore Real Estate Exchange and SRX are trade names of SSPL.

Discover Your Mortgage Savings on mySG Home now.

Monthly Payments

(estimated)

per month

MSR & TDSR REQUIREMENTS

Note: Total Debt Servicing Ratio (TDSR) cannot exceed 60% of your net income. Mortgage Servicing Ratio (MSR) cannot exceed 30% of your income. Calculations are done at 3.5% Interest Rate.

Please contact your mortgage banker for TDSR requirements pertaining to joint borrowers.

- housing loans,

- the refinancing of housing loans, and

- loans secured by property.

The TDSR was introduced to strengthen credit underwriting practices by financial institutions. Loans are only issued to borrowers who can afford them.

For HDB flats and ECs, mortgage repayments must not account for more than 30 percent of a borrowerâs gross monthly income, even if they have no other debt obligations. (See Mortgage Servicing Ratio)