China’s economy slows, hitting a 24-year low. Europe’s economies struggle with disinflation and possibly deflation. Analysts predict that the US dollar will continue to strengthen in 2015.

So what? We live in Singapore.

If you are homeowner or buyer, it matters.

Most floating mortgage rates in Singapore are pegged to the Singapore Interbank Offered Rate (SIBOR), which is the interest rate at which banks offer to lend funds to other banks.

The SIBOR is correlated to the US dollar. Generally as the Singapore dollar weakens against the US dollar, the SIBOR increases and local mortgage rates go up.

Since the US and Europe cut interest rates in 2008 in order to stimulate their economies during the global financial crisis, we have enjoyed rock bottom mortgage rates in Singapore.

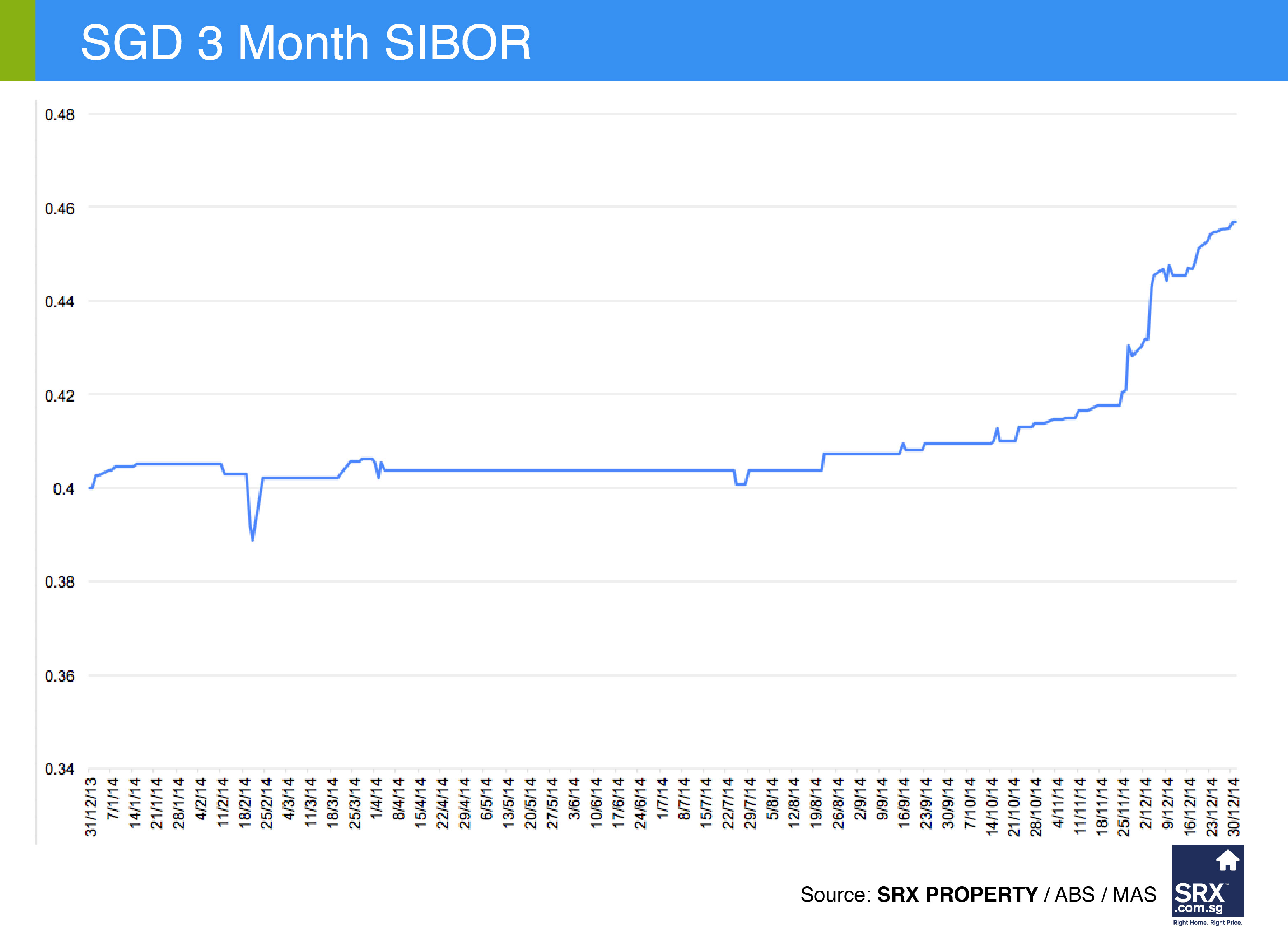

According to MAS, the 3-month SIBOR has gone from a high of 1.88% in September 2008 to a low of 0.25% in September 2011 and hovered in the 0.38-0.42 % range for 2012 through most of 2014.

As a result, during this time, bank interest rates were significantly lower than the HDB loan concessionary interest rate of 2.6%, incentivizing HDB owners and buyers to take out private mortgages in large numbers.

Recently, however, dark clouds have appeared on the horizon. The Singapore dollar has depreciated against the US dollar about 8% since mid-2014. Meanwhile, according to the Association of Banks in Singapore, the 3-month SIBOR closed at 0.65% on 20 January.

How much more can we expect the SIBOR and our mortgage rates to increase in 2015?

There are two schools of thought. Some analysts think that the 3-month SIBOR could increase to 1% or above, believing that the US Federal Reserve will raise interest rates and the Singapore dollar will continue to depreciate due to the global movement to US dollars.

If this turns out to be the case, then we can expect our current private mortgage rates of 1.5-2% to go up.

The other school of thought looks at the world’s struggling economies and is not so sure that the US Federal Reserve and other Central Banks will increase interest rates. They see low inflation in the States, disinflation in Europe, and an upcoming presidential election as reasons for the Federal Reserve to take a pass on raising rates in 2015.

Since no one knows for sure how interest rates will change in 2015, all we can do as homeowners is plan for the worst and hope for the best.

There are three ways that you can inoculate yourself against the possibility of rising mortgage interest rates.

First, when you are in a low interest rate environment, which we are still in, try to lock in the lowest possible mortgage rate for as long a term as you can get.

Second, prepare for the possibility that your monthly mortgage payment will go up by cutting expenses or reallocating savings to cover the increase.

Face it. We have been lucky with relatively low mortgage rates and have spent elsewhere what used to go to our mortgage. If interest rates go up, we need to reallocate those savings back to our mortgage. This can be psychologically painful, but it’s doable.

Third, if you qualify for an HDB loan, then you are faced with a decision. Do you go for the HDB concessionary interest rate or a private bank mortgage which will still provide you significant savings?

Which way you go depends on your tolerance for risk and your cushion of savings.

If your view is that interest rates will not go up much more and you have savings you could put towards your mortgage payments in the event that interest rates go against you, then you should consider taking advantage of the low interest rates in the banking sector.

If you are concerned about rising interest rates or an increase in your monthly payments would put your ability to meet your monthly expenses in jeopardy, then you should consider an HDB loan or a private mortgage that seeks to replicate the HDB loan. For example, POSB offers a floating rate loan that caps the interest rate below the HDB concessionary rate for the first eight years.

Regardless of which direction you end up going, seek out advice from HDB advisors, bankers, and other financial experts. Interest rates go up and they go down. There is always a solution, but it depends on your individual circumstances and is best arrived at by research and working with experts who put your best interest first.