Ogden Nash, the American poet, once wrote, “One rule which woe betides the banker who fails to heed it. Never lend any money to anybody unless they don’t need it.”

This is a humorous way of saying that the only way to minimize risk in the banking business is to lend money to people who already have enough money to pay back the loan.

Of course, in the real world, it doesn't work this way. The economy would grind to a halt if people could not use debt to finance business expansion and household purchases like cars, electronics, and homes. If bankers could lend only to people who don't need it, banks would be out of business.

As such, for the good of the economy and the banks, the latter must lend and assume some level of risk. The trick is to underwrite loans so very few of them default and the risk to the banks, and, thus, the financial system is acceptable.

Underwriting is a fancy way of saying that the banks are trying to figure out whether or not you will repay the loan.

When you apply for a mortgage, the bank will typically consider your credit score, capacity to pay, and the value of the home. These are known as the three “C’s” of mortgage underwriting.

Your credit score accounts for your ability to pay back loans, including credit card debt, car loans, other home mortgages, and personal loans.

Bank underwriters look at your income, existing debt, and your employment history to evaluate your capacity to pay back the loan according to its terms and conditions.

Finally, banks examine the collateral behind the loan, which in the case of a mortgage is the home itself. In the event of default, the bankers want to know that they can resell the property and get their money back. As part of the underwriting process, they will value the home and decide whether or not it has a good chance of holding its value and appreciating.

It is in the interest of policy makers and risk managers to standardize underwriting, as much as possible.

If all the banks are applying the same underwriting rules, it is much easier to measure the risk in their portfolios and take effective actions to safeguard the overall financial stability of the nation.

As such, the Government has standardized parts of Singapore’s collective mortgage underwriting by introducing the Total Debt Servicing Ratio (TDSR). TDSR places restrictions on household debt and stipulates the debt-to-equity ratio, meaning how much cash you need to put down to qualify for a mortgage. This reduces the risk of households overextending themselves financially by taking on a home they cannot afford, especially if interest rates increase.

In addition, automated valuation models (AVM) can help standardize mortgage underwriting. For example, SRX Property’s X-ValueTM is a type of AVM that uses best practices, computer power, and big data to generate estimations of the market value of every home in Singapore.

AVMs are used around the world in mortgage underwriting to provide a standard method for valuing a home. Also, an AVM can be used to test the impact of different market conditions and interest rate scenarios on a bank’s mortgage portfolio.

The standardization of underwriting benefits consumers by making buying, selling, and financing property more transparent and, thus, more predictable. This, in turn, helps foster financial stability within each household.

In the digital age, there are plenty of free resources that help consumers navigate the TDSR rules and benefit from underwriting standardization.

For example, SRX Property offers a free, personalized webapp called my Property Tracker in which you receive free updates on the value of your home and listing and transaction activity in your neighborhood.

By using this secure webapp, you can evaluate the value of your collateral (i.e., your home) as well as use the X-Value calculator to get an estimate of the market value of homes you have shortlisted to buy.

Also, in my Property Tracker webapp, you will find a TDSR calculator that allows you to estimate how much you can borrow given your income.

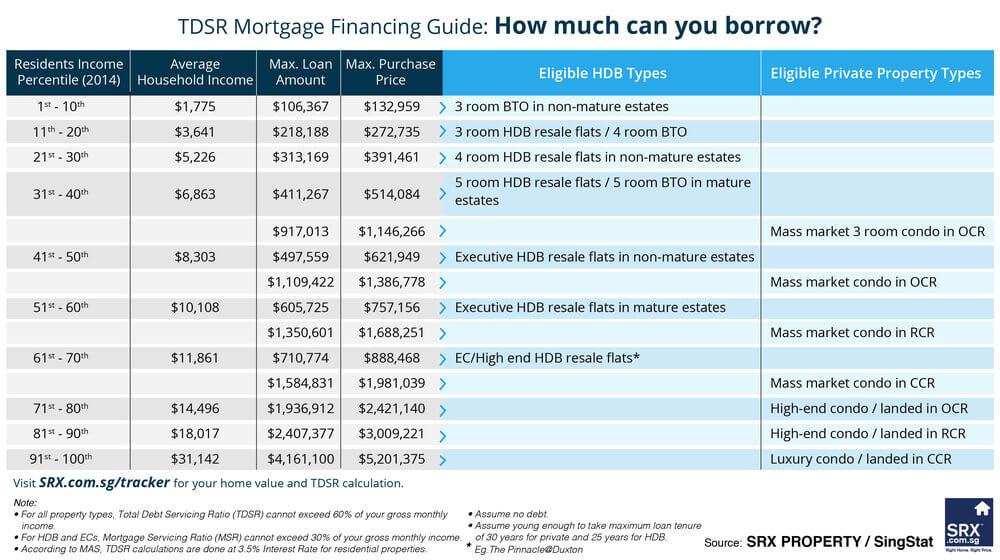

The practical effect of TDSR is that there is a limit on how much most people can borrow. SRX Property Analysts used the TDSR calculator in my Property Tracker to create a TDSR Loan Guide.

While you should do your own calculation to estimate how much you can borrow based on your particular situation, the TDSR Mortgage Financing Guide, gives you a quick understanding of what each income bracket can borrow in terms of maximum loan amount. Based on this number, you can determine your maximum purchase price and the corresponding types of homes.

For example, if your household earns $8,303 per month, you are eligible for a maximum HDB loan amount of $ 497,559. This translates to a maximum purchase price of $621,949, which makes you eligible for Executive HDB flats. (This calculation assumes that you are young enough to take the maximum loan tenure of 25 years for HDB, you can put 20% down, and you have no other debt.)

At the same time, in accordance with TDSR rules, you are eligible for a private loan up to $1,109,422. This translates to a maximum purchase price of $1,386,778, which makes you eligible for a mass market condo in OCR. (This calculation assumes that you are young enough to take the maximum loan tenure of 30 years for a private mortgage, you can put 20% down, and you have no other debt.)

While TDSR does place limits on bank lending, the rules for underwriting and, thus, the rules for buying a home are crystal clear. Now all that is left to do is find the right home at the right price within your specific income segment.

Sam Baker is co-founder of SRX Property, an information exchange formed by leading real estate agencies in Singapore to disseminate market pricing information and facilitate property listings and transactions. To find out the value of your home and how much you can borrow, visit srx.com.sg/tracker.