Singapore's property markets appear to be on the road to nowhere. Lifting the Cooling Measures would put the markets back on the road to recovery. The problem is there's an elephant blocking the way.

Property markets are complex under normal circumstances. Throw in Cooling Measures and we add a new dimension that significantly impacts people’s expectations, the market’s current behaviour and forecasting and planning for the future.

Judging from the latest numbers, Singapore’s property markets are, well, blah.

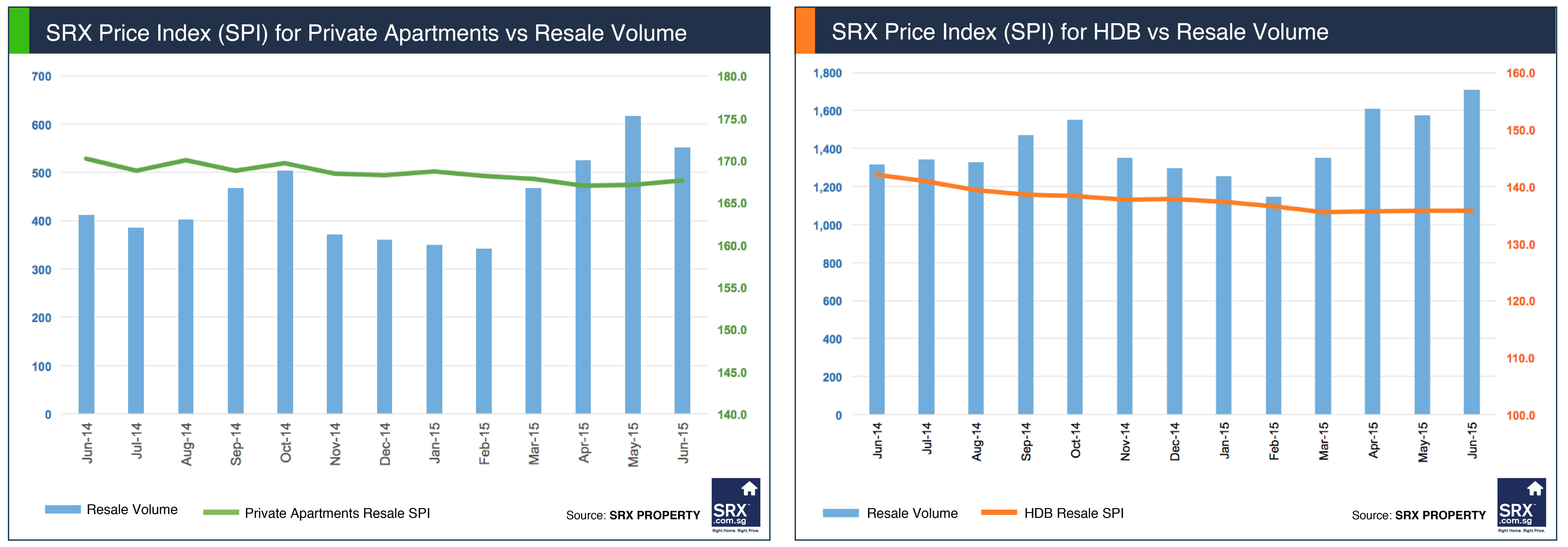

As we see from SRX Property’s monthly flash reports, prices in the private apartment have been flat for one year. Transaction volume in this market is anemic, down 73% since its peak of 2,050 units in April 2010.

As a result of an influx of new supply in the form of Built-to-Orders, the decline in HDB prices have outpaced that of the private market and are down 10.9% since April 2013. Meanwhile, monthly transaction volume is down 53% since its peak in May 2010 and has settled, for about a year now, at a new equilibrium range around 1,500 transactions/month.

If the property markets continue to perform as they have lately, one could be forgiven for wondering if they are on the road to nowhere.

Of course, as connoisseurs of property, all Singaporeans know that lifting the Cooling Measures would put the markets back on the road to recovery.

This is why it’s impossible for any property professional to go to a cocktail party or family gathering without being barraged with a series of questions that begin with, “When’s the Government going to ease the Cooling Measures? After the elections? Will TDSR remain? If the Government eases the stamp duty taxes, by how much? What will be the new rules of the property market in 2016? Is this a good time to buy? To sell? What do I do?”

Answering these questions is impossible for mere mortals because there is a big, fat, sneering elephant standing in the middle of the road to recovery. This elephant is Singapore’s collective portfolio of mortgages.

Under normal circumstances, the mortgage elephant isn't a problem. There are at least five different types of tranquilizer guns that keep him docile and off the roads.

The five barrel combination of a robust economy, low inflation, moderate interest rates, and corresponding income and property asset growth combine to keep the mortgage elephant under control and the financial system stable.

The problem occurs when one of the tranquilizer guns jams (or even backfires) and the docile mortgage elephant turns into a beast. Instead of carrying the load for homeowners by providing them with the means to finance their homes, retirements and dreams, the elephant turns nasty and charges the homeowners, trampling those in his path.

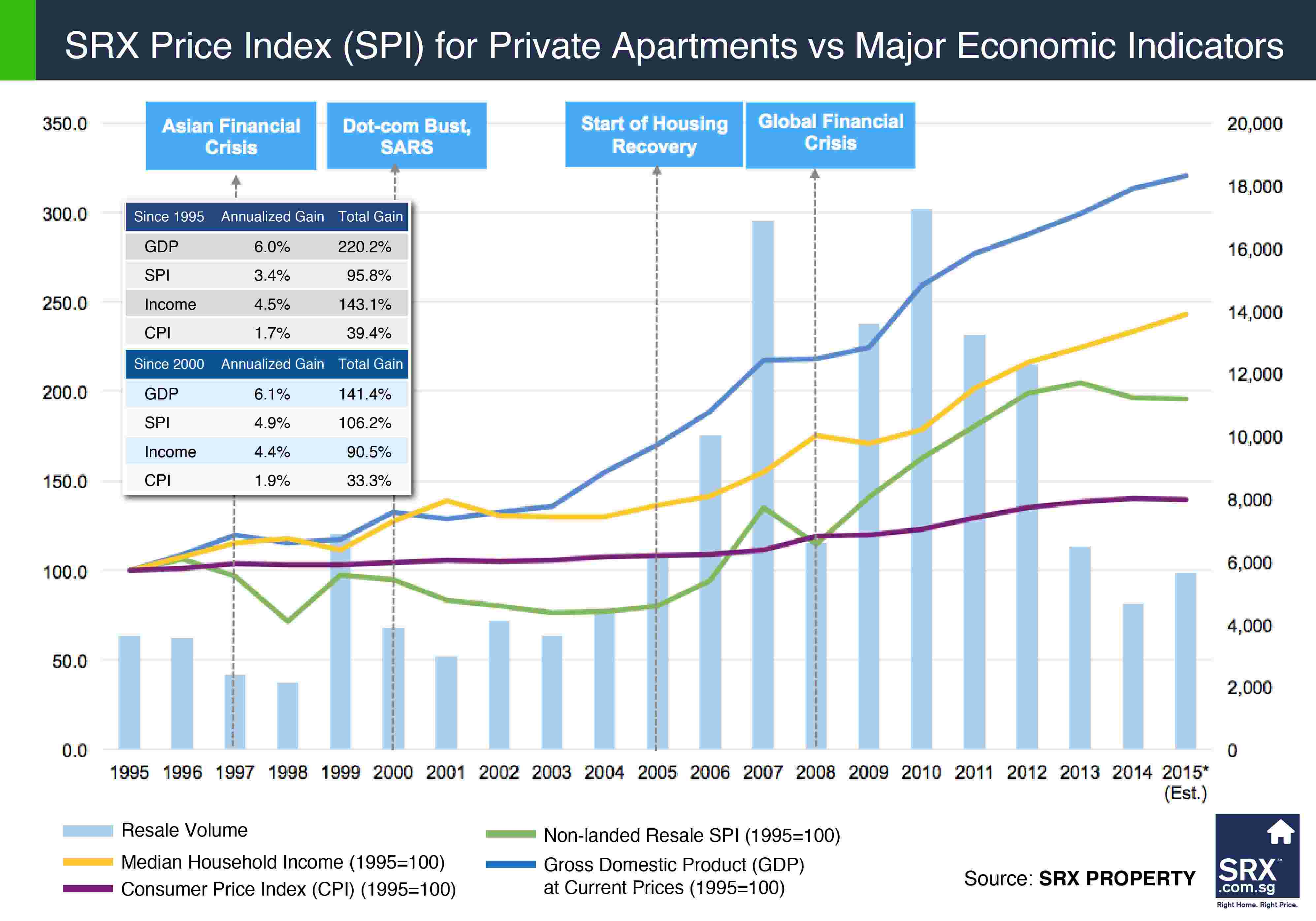

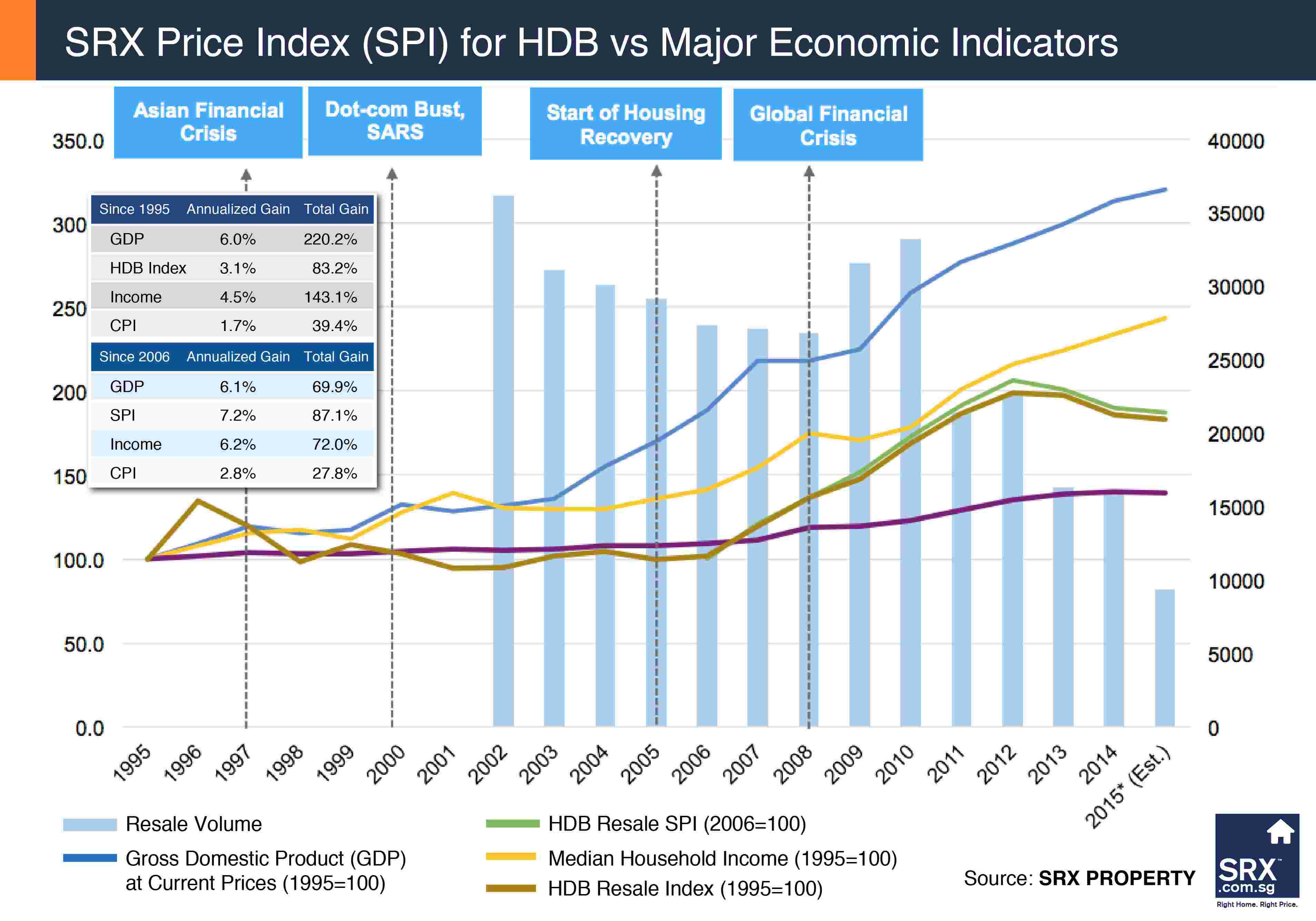

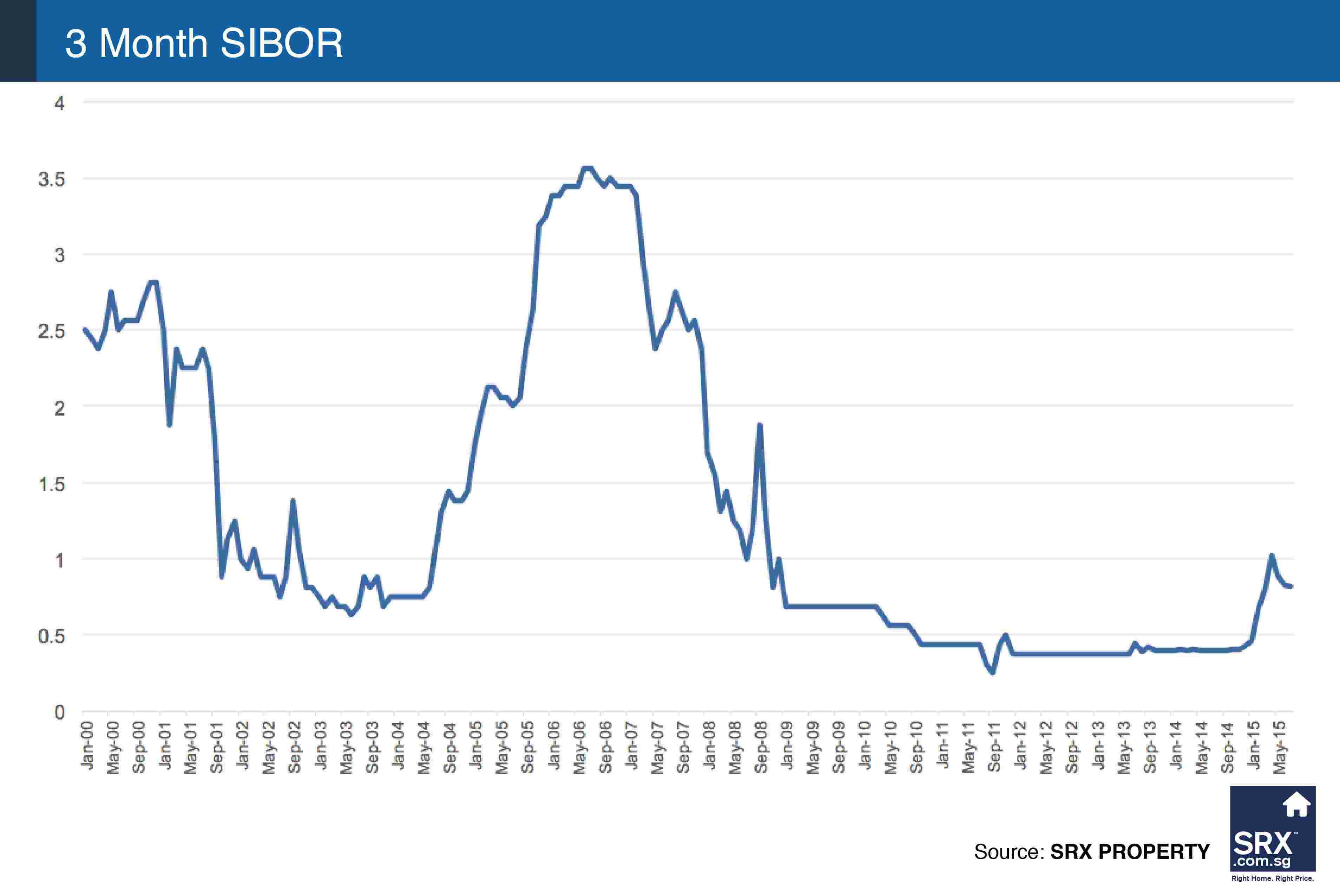

As you can see from SRX Property’s graphics, economic growth, low inflation, and income and property asset growth are not the problem.

It is true that property prices have pulled even and even outpaced income in the last decade or so, but over the long run, property prices have had some distance to catch up. Since 1995, both the Gross Domestic Product (GDP) and median household income have significantly outperformed the property price indices.

While some have argued that supply has not kept pace with population growth, this was not the prime cause of the rapid increase in property prices before and after the Global Financial Crisis (GFC). If supply were the culprit, the Government would have lifted the Cooling Measures by now. Not only has supply kicked in, both the HDB and property markets could be facing oversupply in the next few years. (To validate this hypothesis check out the oversupply in places like Ardmore Park Road and Draycott Drive.)

The real culprit has been historically low interest rates.

The major economies have been bolstering their economies with easy money (i.e., low interest rates) for so long that there are generations of homeowners who have never experienced expensive mortgages. Is it any wonder why Singaporeans have taken advantage of rock-bottom mortgage interest rates to invest in a second or third home?

With the interest rate tranquilizer gun jamming, the mortgage elephant gained weight big time. The banks were tripping over each other to hand out mortgages with the lowest interest rates possible. The mortgage elephant grew some more. The Buyer's Stamp Duty on foreign buyers reduced the overseas competition for Singapore investment properties, which in turn, put downward pressure on property prices and resulted in deep discounts from developers. Singaporeans stepped in to take advantage of these deals. The mortgage elephant grew even bigger and more ornery.

The data and these graphs suggest that the real problem is not housing affordability. Supply - like BTOs - are helping to solve that problem - along with efforts on the economic front to keep the economy humming and improve household income. The real fear is what happens if interest rates increase and borrowers are faced with larger monthly mortgage payments.

Will households have enough money to cover this increase in expenses or will they default? Will the mortgage elephant safely cross the road or will it implode and splatter its blood and guts all over the road to nowhere?

It is not enough to look at graphs of income, GDP, inflation, interest rates, and property price indexes to assess the health of the mortgage elephant. Once one of the tranquilizer guns started to fail, macro analysis went out the window.

The patient - meaning the mortgage elephant – could be in intensive care. Only granular probing and stress testing of the banks' mortgage portfolios will reveal the fragility of the patient and, thus, the financial system.

No doubt that banks and government agencies are hard at work modeling the various interest rate scenarios and their impact on Singapore’s mortgage portfolio and, by extension, the stability of its financial system.

Let’s hope that they are using the most advanced databases and analytic tools to uncover the true health of the mortgage elephant. Once this is known, action can be taken to sedate the mortgage elephant and clear him from the road to nowhere and make way for the road to recovery.